China BD prices hit a year-to-date high in Oct on tight supply, strong demand

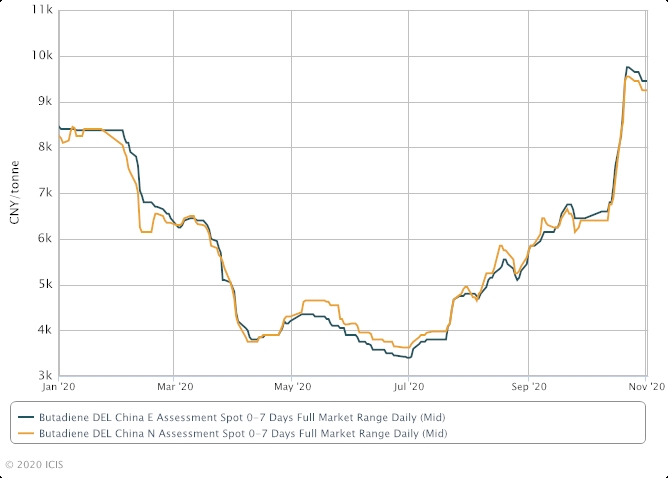

China’s butadiene (BD) prices have been rising after the National Day holiday (1-8 October), hitting a new high so far this year due to tight spot supply and improved downstream demand.

On 23 October, DEL (delivered) prices in east and north China were at yuan (CNY) 9,750/tonne and CNY9,550/tonne respectively, both posting a surge of CNY3,150/tonne from 9 October, ICIS data showed.

The reason behind the price surge was tight spot supply in the domestic BD market, which was caused by a series of factors, including sharp drops in imports, rising exports, lower-than-expected supply from new plants and delayed shipments.

Most market players were previously bearish about domestic BD prices in October, in anticipation of rising output.

Sinopec Zhongke (Guangdong) Refining & Chemical and Sinochem Quanzhou Petrochemical had initially planned to achieve stable operation at their new plants.

This, combined with plant restarts of Nanjing Chengzhi Clean Energy and Jiangsu Sailboat, were expected to exert huge downward pressure on domestic BD prices.

While import prices rose amid tight supply in Asia due to plant maintenance in South Korea and Taiwan.

Thus, most market players believed that domestic BD prices in October would be much lower than import prices.

This put domestic traders and downstream buyers into a very cautious stance toward purchasing imports, which curtailed the import volumes significantly.

China’s BD imports plunged by 57.34% month on month in September, the ICIS Supply and Demand database showed.

Some suppliers sold October-November cargoes in August-September.

Hengli Petrochemical have concluded many export orders since September, taking advantage of the gap between domestic and overseas prices.

A few speculators oversold October cargoes. Therefore, inventories of domestic suppliers, traders and downstream buyers remained at low levels from September.

There were some unexpected disturbance on the supply side. Sinopec Zhongke (Guangdong) Refining & Chemical shut its new plant on 15 October for equipment issues after the start-up. Sinochem Quanzhou Petrochemical merely ran its new plant at around 70% of capacity at the end of October.

Nanjing Chengzhi Clean Energy and Jiangsu Sailboat restarted their plants, but did not produce BD cargoes until mid-to-late October.

Shipments of domestic suppliers were also delayed.

Low inventories and the lower-than-expected supply from new plants led to short spot supply in the domestic market, especially in east China.

However, downstream demand was robust.

After the week-long holiday, synthetic rubber prices rose sharply to a year-to-date high as futures prices for natural rubber hit a two-year high.

Prices for derivatives acrylonitrile-butadiene-styrene (ABS) and other derivatives also surged.

Downstream ABS and rubber latex producers, who enjoyed good orders and lucrative margins, kept their purchases stable.

As the largest BD consumer, some synthetic rubber producers announced on 23 October that they will shut plants or cut run rates to resist surging feedstock prices, which exerted pressure on the BD prices.

- Tireworld Insight: Domestic tire makers eye overseas expansion

- Tireworld Insight: Price disparity severe between China's rubber exports and imports

- Tireworld Insight: China tire exports dependent on US market performance

- Tireworld Insight: SHFE rubber expected to move in tight range in short-term

- Tireworld Insight: Rubber futures to test near-term resistance at 15,000 yuan/tonne

- Tireworld Insight: China’s tire industry on track of rapid growth